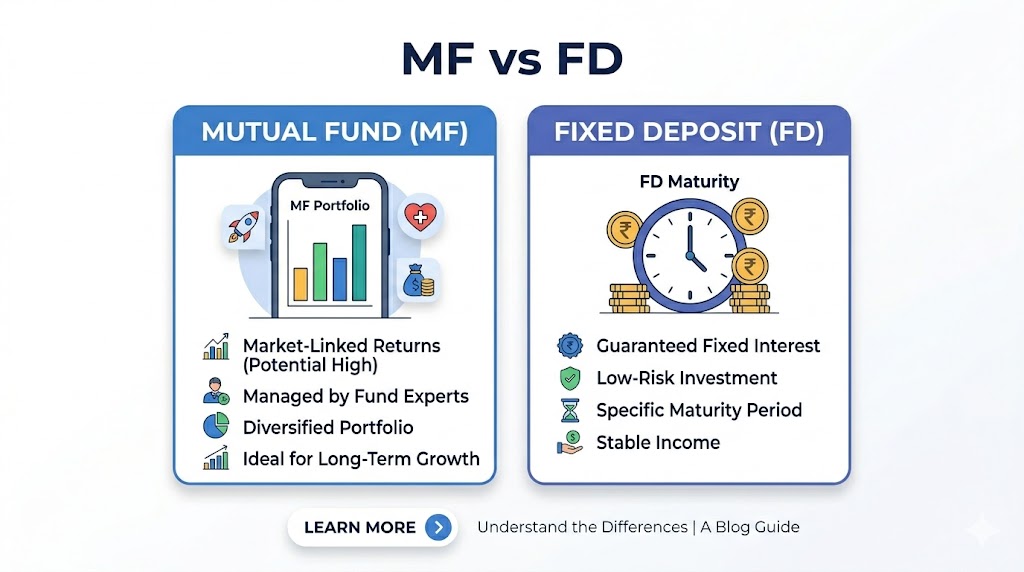

The debate between Mutual Fund vs FD India is a cornerstone of Indian financial planning. For decades, Fixed Deposits (FDs) were the undisputed choice for safe savings. However, in the 2026 economic environment, Mutual Funds (MFs) have gained significant ground due to their potential for inflation-beating returns and the ease of digital investing.

Choosing between a Mutual Fund vs FD India depends entirely on your risk appetite and investment horizon. While an FD offers a guaranteed return and capital safety, Mutual Funds offer the growth needed for long-term wealth creation. This guide breaks down the critical differences to help you park your hard-earned money in the right vehicle.

Who is this for?

This comparison is essential for anyone in India looking to save or invest—from risk-averse individuals seeking peace of mind to aggressive investors aiming for higher growth. It is particularly relevant for those planning for short-term goals (like a vacation) versus long-term goals (like retirement).

Best ways to Mutual Fund vs FD India

The best strategy for Mutual Fund vs FD India is to follow an asset allocation model. For your emergency fund or money needed within 1–2 years, an FD is superior because your principal is safe. For goals that are 5+ years away, Mutual Funds (specifically Equity Funds) are the better choice to ensure your money grows faster than the rate of inflation.

Mutual Fund vs FD India Comparison Table (2026)

Eligibility Criteria

- Residency: Resident Indians, HUFs, and NRIs are eligible for both.

- Documentation: Valid PAN and Aadhaar are mandatory for the KYC process.

- Bank Account: An active savings account in an Indian bank is required.

- Age: Individuals above 18 years; minors can invest through parents/guardians.

Documents Required

- Identity Proof: Aadhaar Card, PAN Card, or Passport.

- Address Proof: Recent electricity bill, telephone bill, or Voter ID.

- Bank Details: Cancelled cheque or bank statement for linking your account.

- KYC Compliance: A digital photograph for e-KYC (common for Mutual Funds).

- The process is governed by the Reserve Bank of India (RBI) guidelines for Video-KYC.

Step by Step Process to Invest

Investing in an FD:

- Log in to NetBanking: Most Indian banks allow instant FD creation online.

- Select Tenure: Choose a period ranging from 7 days to 10 years.

- Enter Amount: Input the sum you wish to deposit.

- Nominee Details: Ensure you add a nominee for the account.

- Confirmation: The amount is debited from your savings account, and an FD receipt is generated.

Investing in a Mutual Fund:

- Download a Fund App: Use a SEBI-registered investment platform.

- Complete e-KYC: Upload your PAN and Aadhaar for instant verification.

- Choose a Fund: Research funds based on your risk (Large Cap, Mid Cap, Debt).

- Select Mode: Choose between a “Lumpsum” (one-time) or “SIP” (monthly) investment.

- Payment: Complete the transaction using UPI or NetBanking.

Tips to Mutual Fund vs FD India faster

To decide faster, look at your “tax bracket.” If you are in the 30% tax bracket, FDs can be very inefficient because the interest is fully taxable at that rate. Mutual funds, especially if held for more than a year, can be significantly more tax-efficient.

Utilize Debt Mutual Funds for Short Term

If you want better returns than an FD but still want lower risk, consider Debt Mutual Funds. In the Mutual Fund vs FD India spectrum, Debt Funds sit in the middle—offering professional management and potentially higher post-tax returns than a traditional bank FD, while remaining much safer than equity markets.

Common Mistakes to Avoid

- Ignoring Inflation: Putting all your money in FDs might result in a “loss of purchasing power” if inflation is higher than the FD rate.

- Panic Selling: Selling your Mutual Funds when the market dips slightly.

- Premature FD Withdrawal: Breaking an FD early often results in a 0.5% to 1% penalty on interest.

- No Diversification: Putting all eggs in one basket. A healthy mix of both is usually best.

Safety Guidelines

When choosing between Mutual Fund vs FD India, remember that Bank FDs are insured up to ₹5 Lakhs per bank by the . For Mutual Funds, ensure you only invest through platforms registered with . Always use your own bank account for transactions and never share your OTP or MPIN with agents promising “guaranteed doubled returns.”

Internal Resources to Improve Your Loan Approval

Frequently Asked Questions

Is a Mutual Fund safer than an FD? No. A Bank FD is considered safer as it offers guaranteed returns and principal protection (up to ₹5 Lakhs), whereas Mutual Fund returns depend on market performance.

Which is better for tax saving, Mutual Fund vs FD India? ELSS (Equity Linked Savings Scheme) Mutual Funds have a 3-year lock-in and offer tax benefits under Section 80C. 5-Year Tax-Saver FDs also offer 80C benefits but often have lower interest rates.

Can I lose money in a Mutual Fund? Yes, since Mutual Funds are market-linked, the value of your investment can go down if the markets perform poorly. FDs do not have this risk.

How do I calculate returns for Mutual Fund vs FD India? For FDs, use the compound interest formula. For Mutual Funds, we look at the CAGR (Compound Annual Growth Rate):CAGR = [(End Value / Start Value)^(1 / Number of Years)] – 1

Conclusion

The choice of Mutual Fund vs FD India isn’t about which is “better” in isolation, but which is better for your specific goal. Use Fixed Deposits for your emergency fund and money you need in the next 24 months. Use Mutual Funds to combat inflation and grow your wealth over the next 5 to 10 years. By balancing the safety of the bank with the growth of the market, you can build a resilient financial future.