Understanding the difference between credit card vs debit card india is one of the most important financial decisions you will make as a modern Indian consumer. In 2026, where digital payments dominate and UPI, RuPay credit cards, and fintech apps are deeply integrated into daily life, choosing the right payment method can significantly impact your financial health.

Both cards may look similar, but they operate on completely different principles. One gives you access to borrowed money, while the other uses your own funds. This guide will break down every aspect of credit card vs debit card india, helping you decide which one suits your needs—and when to use each.

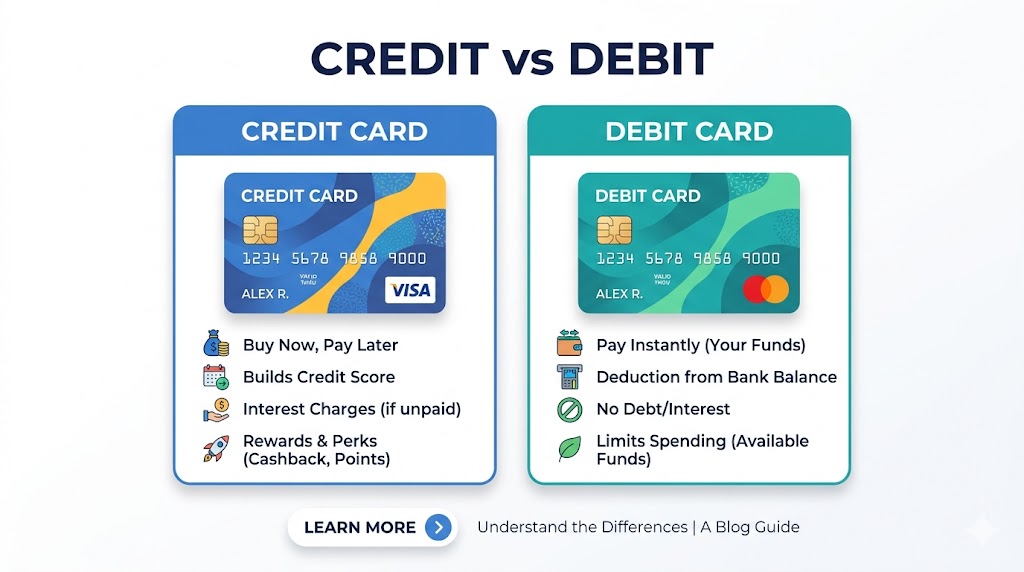

What is a Credit Card?

A credit card is a financial tool that allows you to borrow money from a bank or financial institution up to a certain limit.

Key Features of Credit Cards:

- Pre-approved credit limit

- Interest-free period (typically 45–50 days)

- Rewards, cashback, and loyalty points

- EMI conversion for large purchases

- Builds credit history

Every time you swipe your credit card, the bank pays on your behalf, and you repay later.

👉 Learn more: credit card interest rates india

What is a Debit Card?

A debit card is directly linked to your bank account and allows you to spend only the money you already have.

Key Features of Debit Cards:

- Instant deduction from bank account

- No borrowing or credit involved

- No interest charges

- Easy access via ATMs and POS machines

Debit cards are simple, safe, and ideal for controlled spending.

Credit Card vs Debit Card India: Detailed Comparison

Here’s a comprehensive comparison of credit card vs debit card india:

| Feature | Credit Card | Debit Card |

|---|---|---|

| Source of Funds | Borrowed money | Your own money |

| Interest | Yes (if unpaid) | No |

| Credit Score Impact | Builds score | No impact |

| Rewards | Cashback, points, travel perks | Limited |

| Approval | Requires eligibility | Instant with account |

| Spending Limit | Bank-defined | Account balance |

| Fraud Protection | Strong | Moderate |

| EMI Option | Available | Not available |

This table clearly shows how credit card vs debit card india differs across practical factors.

How Interest Works on Credit Cards

If you fail to pay your full outstanding amount, interest is applied:

Interest=P×R×T

Typical credit card interest rates in India range between 36% – 48% annually.

👉 Official regulatory authority: https://www.rbi.org.in/

This is a critical factor when evaluating credit card vs debit card india.

Advantages of Credit Cards

1. Builds Credit Score

Using a credit card responsibly helps you build a strong CIBIL score, which is essential for:

- Personal loans

- Home loans

- Car loans

2. Rewards and Cashback

Credit cards offer:

- Cashback on spending

- Reward points

- Travel benefits

3. Emergency Financial Support

Credit cards act as a financial buffer during emergencies when you don’t have immediate funds.

4. EMI Conversion

Large purchases can be converted into easy monthly installments.

Disadvantages of Credit Cards

- High interest if dues are not paid

- Risk of overspending

- Late payment penalties

- Hidden charges

👉 Learn more:

credit card charges india

Advantages of Debit Cards

1. No Debt Risk

You can only spend what you have—no borrowing involved.

2. Easy to Use

No approval process, no credit checks.

3. Better Budget Control

Helps you manage spending effectively.

4. No Interest Charges

Unlike credit cards, there is zero interest.

Disadvantages of Debit Cards

- No credit score building

- Limited rewards

- No emergency borrowing

- Less fraud protection compared to credit cards

When to Use Credit Card vs Debit Card India

Understanding when to use each is key.

Use Credit Cards For:

- Online shopping (better protection)

- Large purchases

- Travel bookings

- Building credit score

Use Debit Cards For:

- Daily expenses

- ATM withdrawals

- Budget-controlled spending

- Small transactions

This practical usage strategy simplifies credit card vs debit card india decisions.

Beginner Strategy: Best Approach

If you’re new to financial products:

Step-by-Step Plan:

- Start with a debit card

- Learn spending discipline

- Apply for a beginner credit card

- Use credit card for limited expenses

- Pay full dues every month

👉 Improve approval chances:

improve credit card approval india

This hybrid approach works best in the credit card vs debit card india scenario.

Security Comparison

Credit Card Security

- Chargeback facility

- Fraud protection

- Not directly linked to your bank account

Debit Card Security

- Direct access to bank funds

- Immediate deduction in case of fraud

- Requires careful monitoring

Both are regulated by RBI security norms.

Smart Usage Checklist

✅ Best Practices:

- Always pay full credit card bill

- Keep credit utilization below 30%

- Enable SMS/email alerts

- Avoid using cards on unsecured websites

- Regularly monitor transactions

These habits improve your experience with both card types.

Common Mistakes to Avoid

❌ Credit Card Mistakes:

- Paying only minimum due

- Missing payment deadlines

- Maxing out credit limit

❌ Debit Card Mistakes:

- Ignoring balance tracking

- Using unsafe ATMs

- Sharing OTP or PIN

Avoiding these mistakes is essential in managing credit card vs debit card india effectively.

Long-Term Financial Impact

Credit Cards Help You:

- Build credit history

- Access loans easily

- Get better interest rates

👉 Related:

increase loan eligibility india

Debit Cards Help You:

- Maintain financial discipline

- Avoid unnecessary debt

- Control spending

Both tools serve different financial goals.

Real-Life Examples

Example 1: Salary Day

You receive your salary → Use debit card for essentials.

Example 2: Emergency Expense

Unexpected expense → Use credit card for immediate funds.

Example 3: Online Shopping

Use credit card for rewards and fraud protection.

Example 4: Monthly Budgeting

Use debit card to avoid overspending.

These examples clarify the real-world application of credit card vs debit card india.

Advanced Tips for 2026

- Use RuPay credit cards for UPI payments

- Combine debit and credit strategically

- Track expenses using apps

- Upgrade to premium cards after building history

Credit Card vs Debit Card India: Final Verdict

So which one should you choose?

- Choose debit cards for control and safety

- Choose credit cards for growth and rewards

The smartest approach is to use both wisely.

Final Thoughts

Understanding credit card vs debit card india is essential in today’s financial landscape. Each card has its own strengths, and using them correctly can improve your financial stability and growth.

Start with discipline, build your credit profile, and use both cards strategically to maximize benefits.