Understanding credit card charges india is the most critical step toward mastering your personal finances. While credit cards offer unmatched convenience and rewards, they are also financial products with complex fee structures. In 2026, the Reserve Bank of India (RBI) has implemented stricter transparency rules, ensuring that banks clearly disclose the “Most Important Terms and Conditions” (MITC) to every borrower.

Despite these regulations, many users still fall into debt traps because they overlook “silent” costs. From interest-free periods to the dangers of cash withdrawals, this guide breaks down every credit card charges india component so you can swipe with confidence and avoid unnecessary expenses.

Who is this for?

This guide is designed for every Indian cardholder—from the first-time user with an entry-level card to the seasoned traveler with premium metal cards.

If you’ve ever been surprised by a “Finance Charge” on your statement or want to know the true cost of withdrawing cash from an ATM, understanding credit card charges india will save you thousands of rupees. It is especially vital for those who occasionally carry a balance or use their cards for international transactions.

Best ways to credit card charges india

To avoid the heaviest credit card charges india, you must understand the “Golden Rules” of credit card usage.

Never Pay Only the Minimum Due

Paying the “Minimum Amount Due” is one of the biggest traps in the credit card charges india ecosystem. While it saves you from a late fee, the remaining 95% of your balance immediately starts accruing interest at rates as high as 46% per annum.

Avoid ATM Cash Withdrawals

Cash advances are the most expensive way to use a card. Unlike regular purchases, cash withdrawals have no interest-free period. You are charged a flat fee (minimum Rs. 500) plus high interest from the very second the cash leaves the machine.

Watch the 1% Utility & Rent Fees

In 2026, major banks like ICICI, SBI, and HDFC have introduced a 1% surcharge on utility payments exceeding Rs. 50,000 per cycle and on all rent payments made via credit card. Always check these specific credit card charges india before making large bill payments.

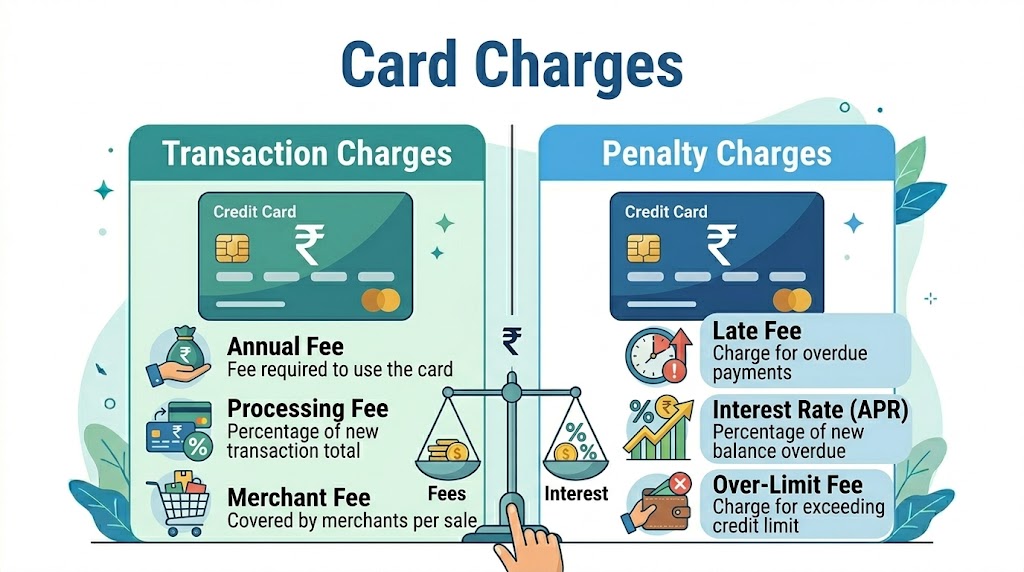

Common Credit Card Charges Comparison (April 2026)

| Charge Type | Standard Rate/Fee | Impact on Your Bill |

|---|---|---|

| Annual/Joining Fee | Rs. 500 – Rs. 15,000 | Charged once a year |

| Finance Charges (Interest) | 3.5% – 3.85% per month | High (up to 46.2% p.a.) |

| Late Payment Fee | Rs. 100 – Rs. 1,300 | Based on amount overdue |

| Cash Advance Fee | 2.5% (Min Rs. 500) | Immediate & High |

| Forex Markup Fee | 1.5% – 3.5% | On international spends |

| Over-limit Fee | 2.5% (Min Rs. 500) | If you exceed your limit |

Eligibility Criteria for Fee Waivers

Many banks allow you to bypass the primary credit card charges india if you meet certain criteria:

- Spend Milestone: Spending Rs. 1 Lakh to Rs. 10 Lakhs annually usually waives the next year’s fee.

- Credit Score: A 780+ CIBIL score can help you negotiate for lower interest rates or premium card upgrades with lower fees.

- Salary Account: Maintaining a salary account with the same bank often leads to “Lifetime Free” (LTF) card offers.

- Digital Profile: Users with a clean repayment history are often eligible for automated fee reversals.

Documents Required to Understand Charges

While you don’t need documents to pay fees, you should keep these digital records to dispute any incorrect credit card charges india:

- Key Fact Statement (KFS): The standardized one-page summary provided by your bank.

- Monthly Statements: To track “Interest-Free” days and periodic surcharges.

- MITC Document: The full list of fees updated by the bank in April 2026.

- Transaction Alerts: SMS or App notifications for real-time charge tracking.

Step by Step Process to Avoid Charges

- Step 1: Set up “Auto-Pay” for the Total Amount Due to eliminate late fees and interest.

- Step 2: Check your statement date. Ensure you clear big spends 2-3 days before the statement is generated to keep your utilization low.

- Step 3: Use the RBI-mandated 3-day grace period if you accidentally miss the due date by a few hours.

- Step 4: For international travel, apply for a “Zero Forex Markup” card to avoid the 3.5% conversion fee.

- Step 5: If you are overcharged, contact the bank’s nodal officer within 30 days for a reversal.

- Step 6: Review your reward points; some banks now charge a “Redemption Fee” of Rs. 99 per request.

Tips to credit card charges india faster

Understand the Interest-Free Period

Most cards offer up to 50 days of interest-free credit. To maximize this and reduce credit card charges india, make large purchases right at the start of your billing cycle.

Consolidate Small Debts

If you are struggling with high interest, consider a personal loan vs credit card loan india comparison. A personal loan at 12% is much cheaper than a credit card’s 46% finance charge.

Monitor UPI-on-Credit Card Rules

In 2026, RuPay credit cards on UPI are common. While most merchant transactions are free for you, some peer-to-peer (P2P) transfers might attract “Small Ticket” credit card charges india. Always check the app prompt before confirming.

Common Mistakes to Avoid

- Withdrawing Cash from ATMs: This is the #1 mistake. The effective interest rate for cash advances can exceed 50% due to the combination of flat fees and daily interest.

- Ignoring GST: Remember that 18% GST is applicable on all credit card charges india, including interest, late fees, and annual fees.

- Missing the Reward Devaluation: Banks frequently update reward rules. If you don’t track them, you might be paying an annual fee for benefits that no longer exist.

Safety Guidelines

The RBI mandates that all credit card charges india must be reasonable and proportionate. Banks cannot increase your credit limit or add “Add-on” services without your explicit consent.

If you encounter arbitrary charges, you have the right to escalate to the RBI Integrated Ombudsman. For the official list of protected borrower rights and 2026 billing standards, visit the Reserve Bank of India website.

Internal Resources to Improve Your Loan Approval

Protect your financial health with these essential resources:

- Learn how to increase loan eligibility india to qualify for lower-interest cards.

- Understand the specific credit card rejection reasons india to avoid failed applications.

- If you are struggling with debt, see how to close personal loan early india to save on interest.

Frequently Asked Questions

What is the most expensive credit card charges india?

Finance charges (interest) and cash advance fees are the most expensive, often reaching an annualized rate of over 46%.

Can I get a late fee waiver?

If it’s your first time missing a due date in several years, most banks will provide a one-time waiver as a “goodwill gesture” if you call their customer care.

Is the 50-day interest-free period always applicable?

No. If you have any outstanding balance from the previous month, you lose the interest-free grace period for all new purchases until the total debt is cleared.

What are the “hidden” credit card charges india?

Common hidden costs include the Reward Redemption Fee (Rs. 99), Fuel Surcharge (1% if not waived), and Dynamic Currency Conversion (DCC) fees when paying in INR abroad.

Conclusion

Mastering credit card charges india is the key to turning your card into a wealth-building tool rather than a debt trap. By paying your bills in full, avoiding cash withdrawals, and staying updated on the latest 2026 RBI guidelines, you can enjoy the perks of credit without the high costs. Remember, transparency is your right, but financial discipline is your responsibility.