Facing a credit card rejection can be frustrating, especially when you feel your finances are in order. In the 2026 Indian banking landscape, algorithms have become more sophisticated, often flagging credit card rejection reasons india that weren’t as critical a few years ago.

Understanding why your application didn’t go through is the first step toward a successful re-application. Banks are not just looking at your income; they are analyzing your digital footprint, your debt-to-income ratio, and even the stability of your current employer. By identifying the specific credit card rejection reasons india, you can take corrective action and secure the plastic you need.

Who is this for?

This guide is for salaried employees, self-employed professionals, and even “New-to-Credit” individuals who have recently faced a setback in their card application.

If you have a stable job but keep getting a “Declined” status, or if you are trying to understand why your high salary wasn’t enough to get a premium card, this breakdown of credit card rejection reasons india will provide the clarity you need to move forward.

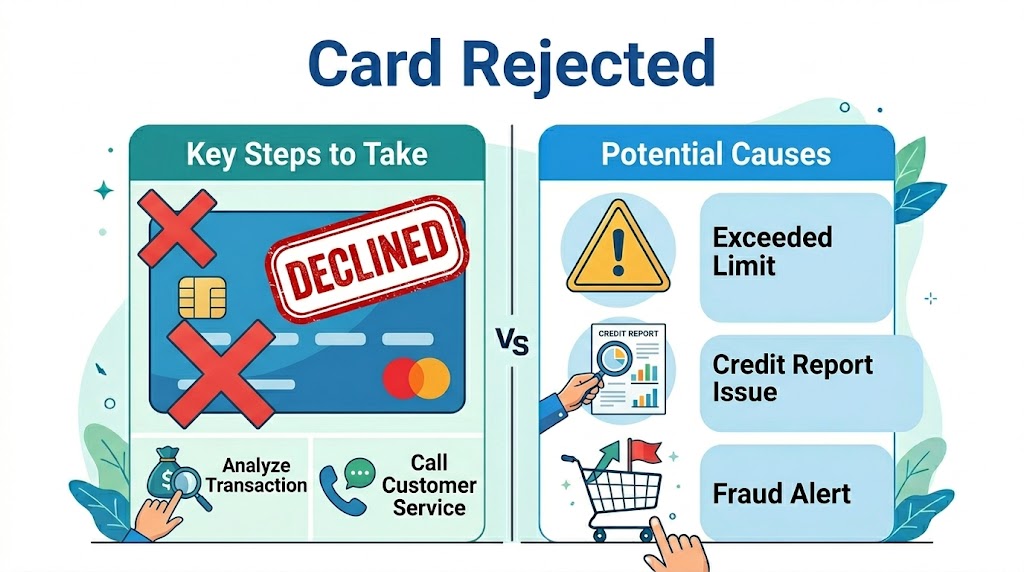

Best ways to credit card rejection reasons india

To avoid a rejection, you must think like a bank’s risk assessment engine.

Address the Credit Score Gap

The most common of all credit card rejection reasons india is a low CIBIL score. In 2026, most banks require a minimum score of 750 for standard cards and 780+ for premium variants. If your score is low, wait six months and improve it before applying again.

Verify Your Office and Home Address

Believe it or not, physical verification is still a major hurdle. If a bank representative finds your office closed or your home address incorrect, it triggers one of the most avoidable credit card rejection reasons india. Always ensure you are present or reachable during the verification window.

Manage Your “Hard” Inquiries

Every time you apply for a card, the bank makes a “hard inquiry” on your credit report. If you apply for five cards in one month, you look desperate for credit, which is one of the top credit card rejection reasons india.

Common Credit Card Rejection Reasons Table (2026)

| Rejection Reason | Severity | Recommended Action |

|---|---|---|

| Low CIBIL Score | High | Improve score by paying small bills on time. |

| Income Below Threshold | High | Apply for a “Basic” or “Entry-level” card. |

| High Existing Debt | Medium | Pay off small personal loans or BNPL debts. |

| Verification Failure | Medium | Ensure someone is available at the provided address. |

| Frequent Applications | Low | Wait for a 3 to 6-month “Cool-off” period. |

Eligibility Criteria

To bypass the most common credit card rejection reasons india, ensure you meet these baseline requirements before clicking apply:

- Age: Between 21 and 65 years.

- Income: Minimum net monthly income of Rs. 20,000 (varies by card).

- Credit History: At least 6 months of history with other loans or cards.

- Location: Must live in a city where the bank has an active presence.

- Employment: Minimum 6 months with the current employer.

Documents Required

Providing clear, verifiable documents can help you avoid the credit card rejection reasons india related to “Document Discrepancy.”

- Identity/Address: Aadhaar and PAN (linked for e-KYC).

- Income: Last 3 months’ salary slips and latest Form 16.

- Bank Statements: Last 6 months’ statement of your primary salary account.

- Employment Proof: A valid company ID or appointment letter.

Step by Step Process to Fix Rejection

- Step 1: Request a formal rejection letter or email from the bank to identify the specific credit card rejection reasons india.

- Step 4: Download your latest CIBIL report to check for any errors or unauthorized entries.

- Step 3: Correct any address or contact details that might have led to a verification failure.

- Step 4: If the reason was “High Debt,” pay off your existing loan against salary india or other small debts.

- Step 5: Wait for at least 90 to 180 days before applying for a new card.

- Step 6: Consider applying for a “Secured Credit Card” (against a Fixed Deposit) to build your profile if you are a first-time user.

Tips to credit card rejection reasons india faster

Check for Pre-Approved Offers

The easiest way to avoid credit card rejection reasons india is to apply for “Pre-approved” offers in your mobile banking app. These are based on your existing relationship and have a 99% approval rate.

Avoid Being in a “Negative Area”

Some banks have a list of “Negative Profiles” or “Defaulter-heavy” pin codes. If you live in such an area, it might be one of the hidden credit card rejection reasons india. Using your office address for communication might help in some cases.

Match the Card to Your Income

Applying for an “Infinite” or “Magnus” card with a Rs. 30,000 salary is a guaranteed way to trigger credit card rejection reasons india. Start with a basic card and upgrade as your income grows.

Common Mistakes to Avoid

- Lying About Income: Banks verify income through your bank statements and EPFO data. If there is a mismatch, it results in an immediate blacklisting.

- Applying with a Poor History: If you have settled a loan in the past, it remains on your report for years and is one of the hardest credit card rejection reasons india to overcome.

- Ignoring Your Credit Utilization: If you are already using 90% of your current card limits, banks see you as a high-risk borrower.

Safety Guidelines

When applying for credit cards, only use official bank websites or verified financial aggregators.

Be cautious of callers who promise “Guaranteed Approval” regardless of your credit history; these are often scams designed to steal your KYC data. For information on your rights as a borrower and how to handle credit disputes, visit the official Reserve Bank of India website.

Internal Resources to Improve Your Loan Approval

If you are struggling with rejections, these resources might help:

- Understand the broader loan rejection reasons india that apply to all credit products.

- If you need funds urgently but can’t get a card, look into a loan without cibil india.

- Learn how to increase loan eligibility india to make your profile more attractive to banks.

Frequently Asked Questions

Will a rejection hurt my CIBIL score?

The rejection itself isn’t recorded, but the “Hard Inquiry” made by the bank stays on your report and can slightly lower your score for a few months.

How long should I wait after a credit card rejection india?

It is highly recommended to wait at least 3 to 6 months before applying for another card to avoid being flagged as a “Credit Hungry” borrower.

Can I get a credit card with a CIBIL score of 600?

It is difficult to get a standard card. Your best option is a “Secured Credit Card,” which is issued against a Fixed Deposit (FD) and does not require a high credit score.

Why was my application rejected despite a high salary?

Salary is only one factor. Other credit card rejection reasons india include a poor credit score, too many active loans, or staying in a “blacklisted” locality.

Conclusion

Understanding the various credit card rejection reasons india is the first step toward financial empowerment. By maintaining a clean credit history, choosing the right card for your income, and ensuring your documentation is flawless, you can turn a “Declined” status into an “Approved” one. Remember, credit is a tool; use it wisely to build a stronger financial future in 2026.