In 2026, the debate between Term vs ULIP India has become more nuanced due to shifting tax laws and RBI/IRDAI digital norms. While term insurance remains the “gold standard” for pure protection, ULIPs have evolved into powerful wealth-creation tools with lower fund management charges and “Wealth Boosters” for long-term stayers. Under the New 2026 Tax Framework, ULIPs now face a 12.5% Long-Term Capital Gains (LTCG) tax if the annual premium exceeds ₹2.5 Lakh, bringing them closer to the taxation level of Mutual Funds.

Choosing between Term vs ULIP India depends entirely on your financial velocity. A term plan is a functional safety net designed to provide a high sum assured at the lowest possible cost, while a ULIP is a seamless hybrid that offers insurance and market-linked growth in one package. By understanding the absolute differences in lock-ins and returns, you can ensure your family’s future is secure without overpaying for features you don’t need.

Who is this for?

This guide is for young professionals, parents, and investors in India. If you are deciding whether to keep your insurance and investments separate or combine them into one reliable digital plan in 2026, this Term vs ULIP India breakdown is for you.

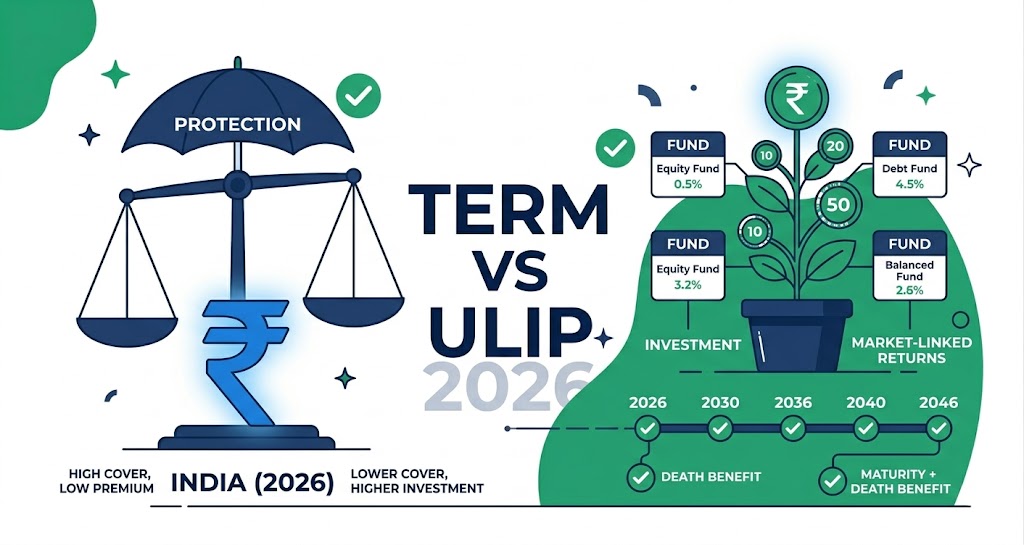

Comparison: Term vs ULIP India (2026)

The 2026 insurance market emphasizes transparency in charges and instant digital issuance.

| Feature | Term Insurance | ULIP (Unit Linked Plan) |

| Primary Purpose | Pure Protection (Death Benefit) | Investment + Protection |

| Maturity Benefit | Zero (Usually Nil) | Fund Value + Sum Assured |

| Premium Cost | Very Low (High Cover) | High (due to Investment) |

| Lock-in Period | None | 5 Years (Mandatory) |

| Tax on Returns | Tax-Free (Section 10(10D)) | 12.5% LTCG (if Premium > ₹2.5L) |

| Market Risk | None | High (Market-linked) |

Key Factors to Consider in 2026

To decide on Term vs ULIP India, prioritize these effective 2026 factors:

1. The Cost of Coverage

Term insurance is the most functional way to get a ₹1 Crore cover for a premium as low as ₹800–₹1,200 per month. In contrast, to get the same ₹1 Crore cover in a ULIP, your premium could be 10x higher because a large portion goes toward buying market units.

2. Lock-in and Liquidity

ULIPs have a mandatory 5-year lock-in. If you need your money back for an emergency before 5 years, your funds are moved to a “Discontinued Policy Fund” earning minimal interest. Term plans have no lock-in because they have no “savings” value—you can stop the policy instantly if you no longer need it.

3. The “Switch” Flexibility

In 2026, ULIPs allow unlimited free switches between Equity and Debt funds. This is a powerful feature for savvy investors to protect their capital during market volatility without paying the capital gains tax that usually triggers when selling Mutual Funds.

Step-by-Step Process to Choose (2026)

- Define Your Goal: If you only need to protect your family’s lifestyle, choose Term Insurance. If you want a disciplined 10-15 year savings goal (like a child’s education), consider a ULIP.

- Check Premium Limits: Stay below the ₹2.5 Lakh annual premium limit in ULIPs to keep your maturity proceeds secure from the 12.5% LTCG tax.

- Digital KYC: Complete your application instantly using the secure Aadhaar-OTP method.

- Verify Identity: Ensure your Aadhaar Bank Linking India is active for seamless premium auto-debits and faster claim processing.

- Review the MITC: Read the “Most Important Terms and Conditions” to check for hidden “Mortality Charges” in ULIPs.

Tips for a Successful Strategy

To make your financial life truly valuable, many experts suggest the “Buy Term and Invest the Rest” (BTIR) strategy. Buy a high-cover term plan and put the saved premium into a low-cost Index Fund or ELSS. Additionally, performing a PAN Card Correction Online India ensures your high-value ULIP investments are correctly reported for tax benefits. If you move, update your Voter ID Status Check India so your physical policy documents and maturity checks reach the correct address securely.

The “Return of Premium” (TROP) Option

In 2026, many term plans offer a “Return of Premium” feature. If you outlive the policy, the bank returns all your premiums paid. While this costs more than a standard term plan, it’s a functional middle ground for those who feel term insurance is a “waste” if they survive.

Common Mistakes to Avoid

- Mixing Goals: Don’t buy a ULIP if you only have a 3-year investment horizon; you will lose money due to front-loaded charges.

- Under-insuring: Because ULIP premiums are high, people often buy low covers (e.g., ₹10 Lakh) that aren’t absolute enough to protect a family.

- KYC Mismatch: Ensure your mobile number matches your Aadhaar Bank Linking India to avoid being flagged by IRDAI’s automated fraud detection.

Safety & Security Guidelines

The IRDAI mandates a “Benefit Illustration” for all ULIPs, showing you projected returns at 4% and 8% interest. When choosing Term vs ULIP India, always look for a “Claim Settlement Ratio” (CSR) of above 98% for the insurer. Never share your “Net Banking” credentials with an agent promising “Guaranteed 20% ULIP returns.”

Internal Resources for Policyholders

- Verify your Voter ID Status Check India for permanent address updates.

- Use Aadhaar Bank Linking India for secure digital KYC.

- Update your PAN Card Correction Online India for accurate tax-saving 80C and 10(10D) reporting.

Frequently Asked Questions

Is ULIP better than Mutual Funds in 2026? ULIPs offer a tax-free “Switch” between funds and included life cover, which Mutual Funds do not. However, Mutual Funds are more liquid as they don’t have a 5-year lock-in.

Which is better for tax saving? Both fall under Section 80C (Old Tax Regime) up to ₹1.5 Lakh. For maturity, Term is always tax-free, while ULIP is tax-free only if the premium is below ₹2.5 Lakh per year.

Can I convert my Term Plan into a ULIP? No, these are separate products. You would need to buy a new ULIP and decide whether to keep or cancel your term plan.

What is the minimum lock-in for ULIP? The IRDAI mandates a minimum lock-in period of 5 years for all ULIPs in India.

Conclusion

Deciding between Term vs ULIP India is a crucial financial choice based on whether you need pure protection or long-term wealth creation. Understanding Term vs ULIP India helps you align your insurance strategy with your life goals, risk appetite, and financial planning needs. In most Term vs ULIP India comparisons, a high-cover term insurance plan remains the top priority for families seeking strong financial security.

When evaluating Term vs ULIP India, term insurance offers maximum coverage at a low premium, making it ideal for income protection. On the other hand, ULIPs combine insurance with investment, making Term vs ULIP India relevant for individuals looking for tax-efficient, market-linked growth over a long horizon.

For most households analyzing Term vs ULIP India, starting with a term plan ensures a solid safety net. If you have surplus funds and a long-term investment horizon of 10+ years, ULIPs can complement your portfolio. Making the right Term vs ULIP India decision involves choosing a trusted insurer, staying disciplined with premium payments, and reviewing performance regularly.

By clearly understanding Term vs ULIP India, you can confidently navigate the 2026 insurance market and build both protection and wealth in a balanced way.