When you need immediate funds, the debate between a personal loan vs credit card loan india is one of the most common financial dilemmas. Both offer unsecured credit without collateral, but the cost, speed, and impact on your long-term financial health differ significantly.

In the 2026 financial market, banks have made it easier than ever to convert your credit limit into a loan, while personal loans have become almost instant thanks to digital verification. Choosing the right one between a personal loan vs credit card loan india depends on whether you value lower interest rates or lightning-fast disbursal.

Who is this for?

This guide is for salaried and self-employed individuals in India who currently hold a credit card or have a stable income.

If you are facing a medical emergency, a home renovation, or a debt consolidation requirement, understanding the personal loan vs credit card loan india landscape will help you avoid high-interest traps and choose a repayment plan that fits your monthly budget.

Best ways to personal loan vs credit card loan india

Choosing the right path requires evaluating your current credit profile and the urgency of your need.

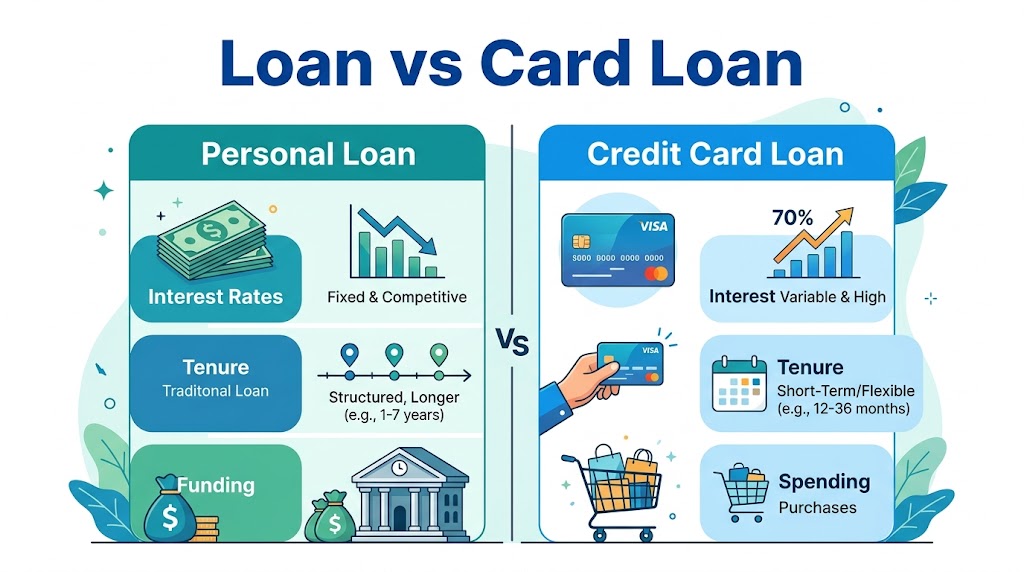

Evaluate the Interest Rate Gap

Typically, in the personal loan vs credit card loan india comparison, personal loans offer lower interest rates (10.5% to 15%) compared to credit card loans (14% to 24%). If you are borrowing a large amount for more than a year, a personal loan is almost always the cheaper choice.

Consider Approval Speed

Credit card loans are often “Pre-approved” based on your existing card limit. In the personal loan vs credit card loan india race for speed, a card loan wins as it often requires zero documentation and provides funds in seconds.

Repayment Flexibility

Personal loans offer longer tenures (up to 5 or 7 years), while credit card loans are generally shorter-term (up to 2 or 3 years). Use this factor to decide which fits your cash flow better.

Personal Loan vs Credit Card Loan Comparison Table (2026)

| Feature | Personal Loan | Credit Card Loan |

| Interest Rate (p.a.) | 10.50% – 18.00% | 14.00% – 24.00% |

| Loan Amount | Up to Rs. 40 Lakhs | Based on Card Limit |

| Approval Time | 2 Hours – 2 Days | Instant (10 Seconds) |

| Tenure | 12 to 72 Months | 6 to 36 Months |

| Processing Fee | 1% to 2% | Flat fee or 1% |

Eligibility Criteria

For a personal loan vs credit card loan india, the requirements vary based on the lender’s existing relationship with you:

- Personal Loan: Minimum salary of Rs. 25,000, 750+ CIBIL score, and at least 1 year of employment.

- Credit Card Loan: Must be an existing cardholder with a good repayment track. No fresh income proof is usually needed.

- Common Requirement: You must be between 21 and 60 years of age and a resident of India.

Documents Required

One major difference in the personal loan vs credit card loan india debate is the documentation.

- Personal Loan: PAN, Aadhaar, last 3 months’ salary slips, and 6 months’ bank statements.

- Credit Card Loan: Usually zero documents required if you apply through your bank’s mobile app.

- Digital Signature: Both require an Aadhaar-based OTP for the final agreement.

Step by Step Process to Apply

- Step 1: Check your mobile banking app for any “Pre-approved” credit card loan offers.

- Step 2: Compare the interest rate offered on your card against current market rates for a personal loan vs credit card loan india.

- Step 3: If you choose a personal loan, upload your income documents for digital verification.

- Step 4: Complete the Video-KYC if prompted by the bank.

- Step 5: E-sign the loan agreement and set up the auto-debit (e-NACH).

- Step 6: Receive funds in your savings account.

Tips to personal loan vs credit card loan india faster

Check Your “Blocked” vs “Open” Limit

Some credit card loans block your existing credit limit, while others are “over and above” your limit. Understanding this is crucial in the personal loan vs credit card loan india decision, as a blocked limit reduces your ability to use the card for daily spends.

Leverage Your Banking Relationship

If you apply for a personal loan at the bank where you have a salary account, your personal loan vs credit card loan india experience will be much faster, often matching the speed of a card loan.

Look for Processing Fee Waivers

During festive seasons, banks often waive processing fees for personal loans, making them significantly cheaper than credit card loans.

Common Mistakes to Avoid

- Focusing Only on Monthly EMI: A credit card loan might have a smaller monthly EMI due to a smaller loan amount, but the interest rate is usually much higher.

- Ignoring Credit Utilization: A credit card loan can increase your credit utilization ratio, which might temporarily dip your CIBIL score.

- Missing the Fine Print on Foreclosure: Check if you can pay off the loan early without penalties.

Safety Guidelines

Whether you opt for a personal loan vs credit card loan india, ensure you are dealing with an RBI-regulated bank or NBFC.

Never share your Credit Card CVV, Expiry Date, or PIN with anyone claiming to offer a “low-interest loan.” Legitimate banks will only require an OTP for the transaction. For more information on secure digital borrowing, visit the official Reserve Bank of India website.

Internal Resources to Improve Your Loan Approval

Enhance your financial strategy with these essential guides:

- Understand loan rejection reasons india to avoid common application pitfalls.

- Learn how to increase loan eligibility india to secure a lower interest rate.

- Use a loan emi calculator india to compare the total cost of both options before deciding.

Frequently Asked Questions

Is the interest rate fixed for a personal loan vs credit card loan india?

Yes, most personal loans and credit card loans in India come with a fixed interest rate, meaning your EMI remains the same throughout the tenure.

Can I get a credit card loan if I don’t have a credit card?

No, a credit card loan is specifically for existing cardholders. If you don’t have a card, a personal loan or a loan against salary india is your best bet.

Which is better for a small amount: personal loan vs credit card loan india?

For small amounts (under Rs. 50,000) that you can repay quickly, a credit card loan is often more convenient due to the lack of paperwork.

How does a loan affect my credit card limit?

If the loan is “within the limit,” your available credit for shopping will decrease by the loan amount. As you pay EMIs, your limit is gradually restored.

Conclusion

The personal loan vs credit card loan india choice comes down to a balance of cost and convenience. If you need a large sum and want the lowest interest rate, a personal loan is the superior choice. However, for instant, small-ticket requirements where speed is the only priority, a credit card loan offers unmatched ease. Always calculate the total interest outgo before making your final decision.