Experiencing a loan rejection due to low salary India 2026 is a common hurdle, especially as the RBI has recently tightened risk regulations for unsecured lending. In 2026, lenders are not just looking at the total amount you earn, but your “disposable income”—what remains after your current expenses and existing debts. If your net monthly pay is below ₹15,000 to ₹25,000, traditional banks like HDFC or ICICI may categorize you as high-risk. However, rejection isn’t the end of the road; it simply means you need to adjust your borrowing strategy to match your profile. [Check Your Loan Eligibility]

The primary technical reason for loan rejection due to low salary India 2026 is a high Fixed Obligation to Income Ratio (FOIR). Most Indian lenders prefer your total monthly debt payments (including the potential new loan) to stay below 40% to 50% of your take-home pay. If you already have a couple of small EMIs, your FOIR might already be at the limit, triggering an automatic rejection regardless of your credit score.

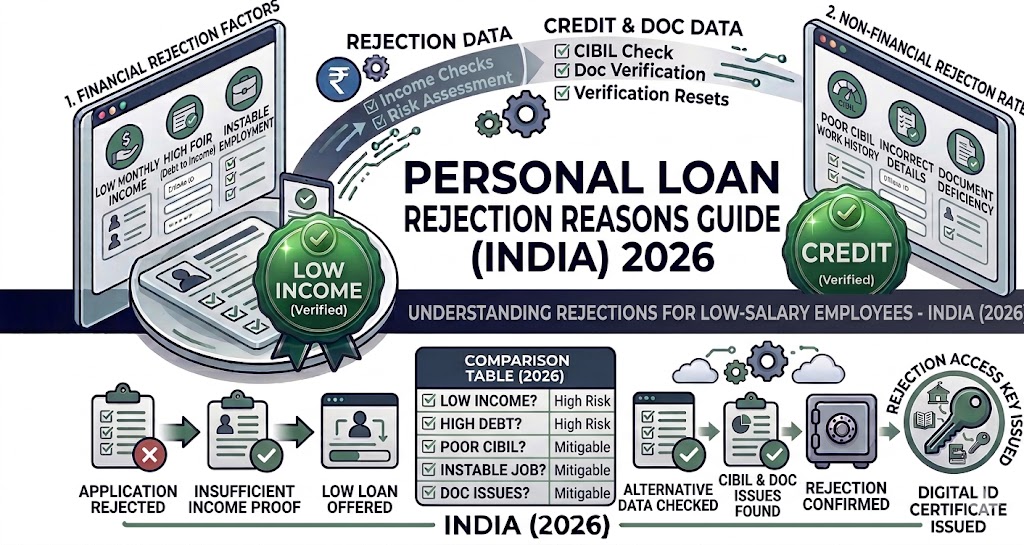

Top Reasons for Loan Rejection due to low salary in 2026

Understanding why a loan rejection due to low salary India 2026 occurs can help you fix your application for next time:

- High FOIR: Your existing debt obligations consume too much of your monthly income.

- City-Specific Minimums: In Tier-1 cities like Mumbai or Delhi, lenders often set the minimum salary at ₹25,000, whereas Tier-2 cities might accept ₹15,000.

- Unstable Employment: Lenders prefer at least 6–12 months of continuous service with your current employer.

- Credit Score Gap: A low salary combined with a CIBIL score below 700 is a major red flag for unsecured loans for loan rejection due to low salary India.

5 Solutions to Fix a Rejection

If you’ve faced a loan rejection due to low salary India 2026, use these strategies to improve your approval chances:

- Add a Co-Applicant: Apply with a spouse or parent who has a steady income. Lenders will consider your combined income, significantly lowering your FOIR.

- Choose the Right Lender: Switch from big banks to NBFCs or Fintech apps. Platforms like Fibe, KreditBee, or MoneyView often accept salaries as low as ₹12,000 to ₹15,000.

- Clear Small Debts: Pay off a small credit card bill or an old consumer durable EMI. Even removing a ₹2,000 monthly obligation can unlock a much higher loan amount.

- Opt for a Longer Tenure: Increasing your tenure reduces the monthly EMI, which may bring your application back within the lender’s acceptable FOIR range.

- Secure the Loan: If unsecured personal loans fail, try a Gold Loan or a Loan Against Fixed Deposit. These have virtually no minimum salary requirements because they are backed by collateral.

Best Lenders for Low Salary Profiles (2026)

| Lender Type | Typical Min. Salary | Approval Chance | Best For |

| Fintech Apps (Fibe/Navi) | ₹12,000 | High | Instant micro-loans (₹10k–₹2L) |

| Regional NBFCs | ₹15,000 | Medium | Mid-sized loans (₹1L–₹5L) |

| Public Sector Banks (SBI) | ₹15,000 | Medium | Low interest rates for govt employees |

| Private Banks | ₹25,000 | Low | Premium employees with high scores |

Internal Resources

FAQ Section

1. What is the minimum salary for a personal loan in 2026?

While it varies, most fintechs start at ₹12,000, whereas major private banks usually require a minimum of ₹25,000 net monthly income.

2. Can I get a loan if my salary is paid in cash?

It is extremely difficult to get a loan with a cash salary. Lenders in 2026 require digital proof via bank statements. Consider depositing your cash into a bank account regularly to build a “verifiable” income history for loan rejection due to low salary India.

3. Does a low salary automatically mean a low loan amount?

Not necessarily. You can get a higher amount by choosing a longer tenure or adding a co-applicant to increase the total income considered by the bank.

4. How many months should I wait after a rejection?

Wait at least 3 to 6 months before reapplying. Multiple “Hard Inquiries” in a short period can further damage your credit score.

Conclusion

A loan rejection due to low salary India 2026 is often just a sign that you are knocking on the wrong door. By shifting your focus to fintech lenders, reducing your existing debt, or applying with a co-borrower, you can effectively bridge the income gap. Always verify your FOIR using an online calculator before applying to ensure your profile meets the lender’s safety standards.