Navigating the various Types of Insurance Policies India is a fundamental step toward building a robust financial plan in 2026. Insurance in India serves as a crucial safety net, designed to protect individuals, families, and businesses from unexpected financial losses. With the Insurance Regulatory and Development Authority of India (IRDAI) continuously introducing customer-centric reforms, the market offers a diverse array of products tailored to every stage of life.

Understanding the fundamental Types of Insurance Policies India allows you to make informed decisions about protecting your life, health, assets, and liabilities. This guide provides a comprehensive overview of the primary insurance categories, their specific purposes, and how to choose the right coverage for your unique needs.

Who is this for?

This guide is essential for every adult in India, including salaried professionals, self-employed individuals, business owners, and retirees. Whether you are looking to protect your family’s future, secure your health, or safeguard your valuable assets like a car or home, this resource simplifies the complex world of insurance.

Best ways to Types of Insurance Policies India

The best way to approach Types of Insurance Policies India is to start with a thorough needs analysis. Prioritize protection based on potential financial impact: Life insurance for dependents, Health insurance for medical emergencies, and Motor insurance as a legal requirement. For other assets or specific situations (like travel), evaluate the risk and choose specialized policies accordingly. Leveraging digital platforms for comparison is highly effective.

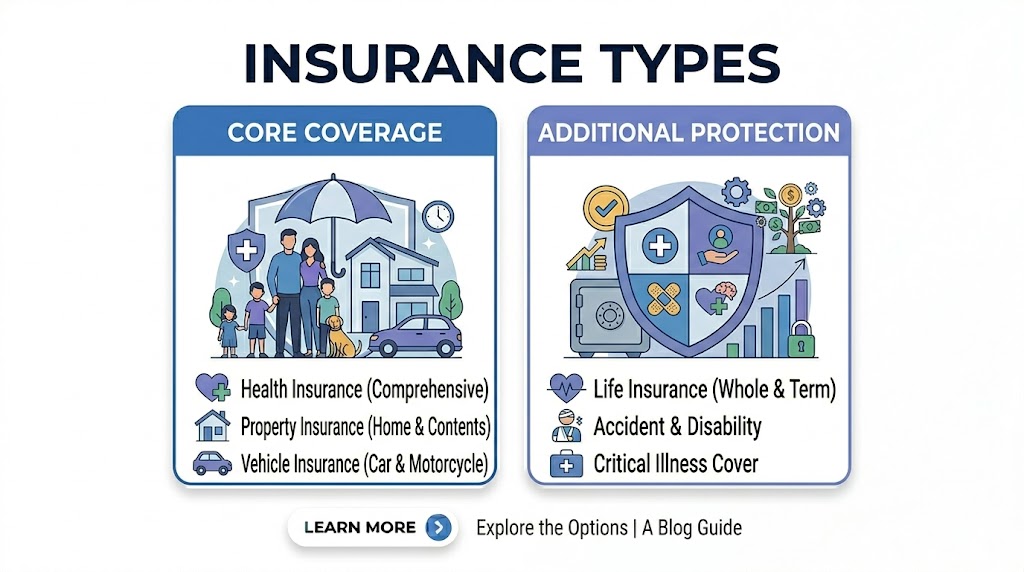

Types of Insurance Policies India Comparison Table (2026)

| Insurance Type | Primary Goal | Mandatory? | Key Benefit |

| Life Insurance | Financial security for dependents | No | Death Benefit |

| Health Insurance | Covers medical expenses | No | Cashless Hospitalization |

| Motor Insurance | Damage to vehicle/Third-party | Third-Party is Mandatory | Financial protection from accidents/theft |

| Travel Insurance | Unexpected travel risks | Often (Depends on Destination) | Covers trip cancellation, medical emergencies abroad |

| Home Insurance | Damage to property/contents | No | Covers natural disasters, theft |

Eligibility Criteria

- Age: Min 18 for most policies as a proposer. Entry age varies (e.g., up to 65 for health).

- Resident Status: Indian residents and, in many cases, Non-Resident Indians (NRIs).

- Health: Medical check-ups might be required for life and health insurance, especially at higher ages or coverage amounts.

- Asset Ownership: Valid ownership documents for motor, home, or other property insurance.

- Income/Profession: For certain high-cover life insurance policies.

Documents Required

- Identity Proof: Aadhaar Card, PAN Card, Voter ID, or Passport.

- Address Proof: Recent utility bill, rent agreement, or bank statement.

- Income Proof (Life/High Health): Salary slips, ITR, or bank statements.

- Age Proof: Birth Certificate, 10th/12th Marksheet, or Passport.

- Asset Documents: Vehicle Registration Certificate (RC) for motor insurance; Property documents for home insurance.

- Recent Photographs: Passport-sized.

Step by Step Process to Apply

- Identify Needs: Determine which Types of Insurance Policies India you genuinely require.

- Research & Compare: Use online comparison portals to evaluate plans based on cover, premiums, and features.

- Choose an Insurer: Select a reputable company with a strong Claim Settlement Ratio (CSR).

- Fill Application Form: Provide accurate personal, medical (if applicable), and asset details.

- Upload Documents: Submit digital copies of the required proofs.

- Pay Premium: Use secure online payment methods.

- Underwriting: The insurer assesses the risk (may include medical tests).

- Policy Issuance: Receive the digital policy document (e-policy).

Tips to Types of Insurance Policies India faster

To expedite the application process for any of the Types of Insurance Policies India, leverage insurers offering instant online policies with e-KYC. Ensuring all your documents are digitally scanned and readily available is crucial.

Buy Online for Speed and Savings

Purchasing your insurance policies online is not just faster but often cheaper. Direct online purchases eliminate intermediary commissions, and the entire process—from comparison to payment and policy issuance—can often be completed in a single session, making it the most efficient way to secure coverage.

Common Mistakes to Avoid

- Underinsurance: Choosing a sum insured that is insufficient to cover actual losses.

- Non-Disclosure: Hiding pre-existing medical conditions or relevant facts.

- Ignoring Fine Print: Not reading the policy exclusions and terms thoroughly.

- Choosing Solely on Premium: Overlooking critical features for a slightly lower cost.

- Delayed Renewal: Letting policies lapse, leading to a break in coverage and loss of benefits.

Safety Guidelines

Always purchase insurance from companies duly registered with the Insurance Regulatory and Development Authority of India (IRDAI). When exploring Types of Insurance Policies India, protect your personal and financial information. Only share sensitive data through secure, official channels. Be wary of unsolicited offers and verify any agent’s credentials on the IRDAI website. Review the policy document during the “Free-Look Period” (usually 15-30 days) to ensure it meets your expectations.

Internal Resources to Improve Your Loan Approval

- Learn how Pre-approved Personal Loan in India works.

- Understand NBFC vs Bank Loan India differences.

- Discover benefits of Loan EMI Calculator Guide India.

Frequently Asked Questions

Which insurance is mandatory in India?

Third-party motor insurance is mandatory for all vehicles under the Motor Vehicles Act. While not legally mandatory, health and life insurance are highly recommended for financial security.

Can I have multiple health insurance policies?

Yes, you can hold multiple health policies. However, the total claim cannot exceed the actual hospitalization expense, and policies might have ‘contribution clauses’.

How can I reduce my insurance premium?

You can lower premiums by opting for a higher deductible (in health/motor), maintaining a good credit score (sometimes considered), installing safety devices (motor/home), and purchasing when young (life/health).

What is the ‘Claim Settlement Ratio’ (CSR)?

CSR indicates the percentage of claims a company settles out of the total claims received. A higher CSR generally suggests better reliability.

Conclusion

Understanding the diverse Types of Insurance Policies India empowers you to proactively manage risk and build a secure financial future for yourself and your loved ones. Whether it is protecting your family with life insurance, safeguarding your health, or securing your valuable assets, there is a policy tailored to every need. By prioritizing essential coverage, comparing plans diligently, and choosing regulated insurers, you can confidently navigate the complexities of insurance and ensure that you are protected against life’s uncertainties.