Deciding between a secured vs unsecured credit cards india is often the first major choice in a borrower’s credit journey. While the physical cards look identical, the underlying mechanism for approval and the risk for the bank are vastly different. In the 2026 financial market, both types serve distinct purposes, whether you are trying to rebuild a damaged score or leverage your high income for luxury perks.

Understanding the nuances of secured vs unsecured credit cards india is crucial because one requires an upfront investment, while the other relies entirely on your reputation and repayment history. Choosing the wrong one could lead to unnecessary rejections or locked-in liquidity.

Who is this for?

This guide is for everyone from students and “New-to-Credit” individuals to high-earning professionals.

If you have been rejected due to a low CIBIL score, a secured card is your path to recovery. If you have a stable job and a score above 750, comparing secured vs unsecured credit cards india will help you understand why you should skip the collateral and go straight for premium unsecured offerings.

Best ways to secured vs unsecured credit cards india

The right choice depends on your current “Credit Health” and financial liquidity.

Start Secured to Build a Foundation

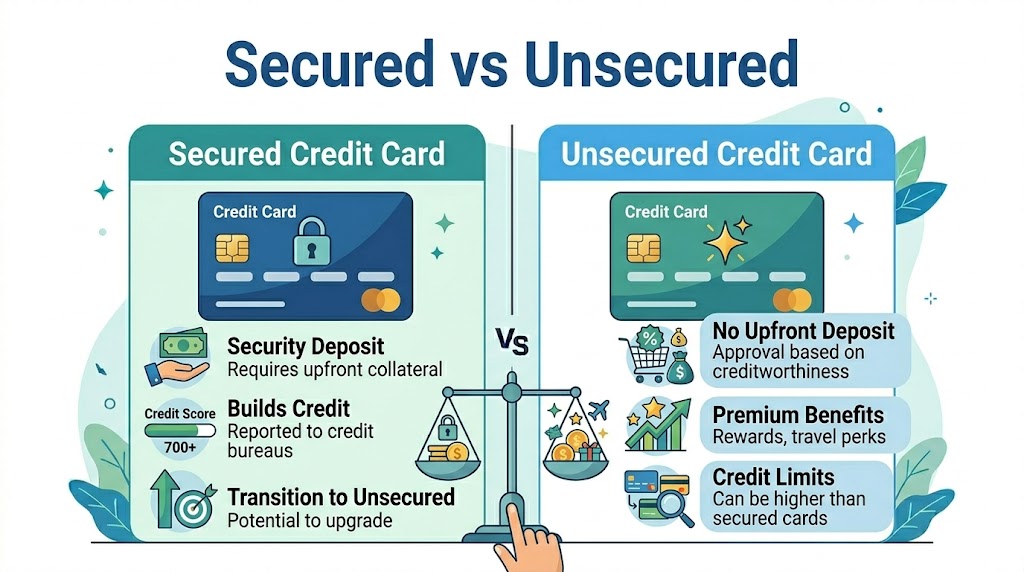

If you have zero credit history, a secured card is the best way to improve credit card approval india for future products. You open a Fixed Deposit (FD) with a bank, and they issue a card with a limit usually equal to 80-90% of that FD.

Transition to Unsecured for Rewards

Once your score is healthy, an unsecured card is the winner in the secured vs unsecured credit cards india debate. These cards offer higher limits, better reward points, and airport lounge access without requiring you to lock your money in a deposit.

Evaluate Risk vs. Reward

With a secured card, if you default, the bank simply takes the money from your FD. With an unsecured card, a default leads to aggressive recovery and a massive hit to your CIBIL score.

Secured vs Unsecured Comparison Table (April 2026)

| Feature | Secured Credit Card | Unsecured Credit Card |

|---|---|---|

| Collateral Required | Yes (Fixed Deposit) | No (Based on Income) |

| Credit Score Need | Nil / Very Low | High (750+) |

| Interest Rates | Slightly Lower | Standard (36-42% p.a.) |

| Approval Speed | Instant | 2 – 7 Days |

| Credit Limit | 80-90% of FD Value | Based on Salary/Income |

Export to Sheets

Eligibility Criteria

The eligibility for secured vs unsecured credit cards india highlights the difference in risk:

- Secured Cards: Almost anyone over 18 with a valid PAN/Aadhaar and a minimum FD (usually Rs. 5,000 to Rs. 20,000).

- Unsecured Cards: Requires a steady monthly income (Rs. 25,000+), a good CIBIL score, and often a stable employment history.

- Documentation: Both require standard KYC, but unsecured cards demand proof of income (Salary slips/ITR).

Documents Required

The document trail for secured vs unsecured credit cards india varies by complexity.

- Secured Card: Just your Aadhaar, PAN, and the FD receipt. Often no income proof is asked.

- Unsecured Card: Aadhaar, PAN, 3 months’ salary slips, and 6 months’ bank statements.

- Digital KYC: Both typically use Video-KYC for instant onboarding.

Step by Step Process to Apply

- Step 1: Assess your credit score. If it’s below 700, look for a secured card.

- Step 2: For a secured card, open a digital FD through the bank’s app.

- Step 3: For an unsecured card, compare the personal loan interest rates india to see if the bank’s other credit products are competitive.

- Step 4: Submit your digital application and complete the Video-KYC.

- Step 5: For unsecured cards, wait for the physical or digital verification of your office/home address.

- Step 6: Receive your card and activate it via the mobile app.

Tips to secured vs unsecured credit cards india faster

Use “Step-UP” Secured Cards

Some Fintechs offer “Step-UP” cards that start with a small FD and allow you to increase the limit as you pay on time, effectively bridging the gap between secured vs unsecured credit cards india.

Leverage Existing FDs

If you already have a Fixed Deposit for savings, check if your bank can issue a card against it. This is the fastest way to get a secured card with zero new paperwork.

Avoid Multiple Unsecured Applications

If you apply for multiple unsecured cards and get rejected, your score will drop further. In the secured vs unsecured credit cards india strategy, it is better to take one secured card and use it for 6 months to guarantee an unsecured approval later.

Common Mistakes to Avoid

- Closing the FD of a Secured Card: If you close the FD, the card is cancelled immediately. This can hurt your “Credit Age.”

- Treating Secured Cards Casually: Just because there is an FD doesn’t mean you can skip payments. Late payments on secured cards still damage your CIBIL score.

- Ignoring Annual Fees: Both types can have annual fees. Ensure the rewards justify the cost, especially for unsecured premium cards.

Safety Guidelines

Whether you choose a secured or unsecured card, always apply through RBI-regulated entities.

Be wary of apps that promise an unsecured card to someone with a 500 CIBIL score in exchange for a “processing fee.” These are scams. Genuine banks only charge fees after the card is issued, usually in the first statement. For more on credit safety and your rights, visit the official Reserve Bank of India website.

Internal Resources to Improve Your Loan Approval

Further your credit knowledge with these essential guides:

- Learn how to increase loan eligibility india for better unsecured card offers.

- If you’ve been rejected, understand the specific credit card rejection reasons india.

- New to credit? Read our guide on getting a loan without cibil india.

Frequently Asked Questions

Can I convert a secured card into an unsecured one?

Most banks do not offer direct conversion. You usually have to apply for a new unsecured card once your score improves and then close the secured one.

Is the credit limit higher on secured vs unsecured credit cards india?

Initially, unsecured cards often have higher limits if you have a high salary. However, a secured card’s limit is only limited by the size of your Fixed Deposit.

Does a secured card help my CIBIL score?

Yes. Banks report secured card repayments to CIBIL exactly like unsecured ones. It is one of the most effective ways to build a score from scratch.

Which is better for international travel?

Unsecured premium cards generally offer better forex markups and international lounge access compared to basic secured cards.

Conclusion

The secured vs unsecured credit cards india choice is a strategic one. If you are starting fresh or fixing past mistakes, the secured card is your best friend. If you have a proven track record, the unsecured card offers the rewards and financial freedom you deserve. Evaluate your needs, check your score, and choose the tool that best serves your financial future in 2026.