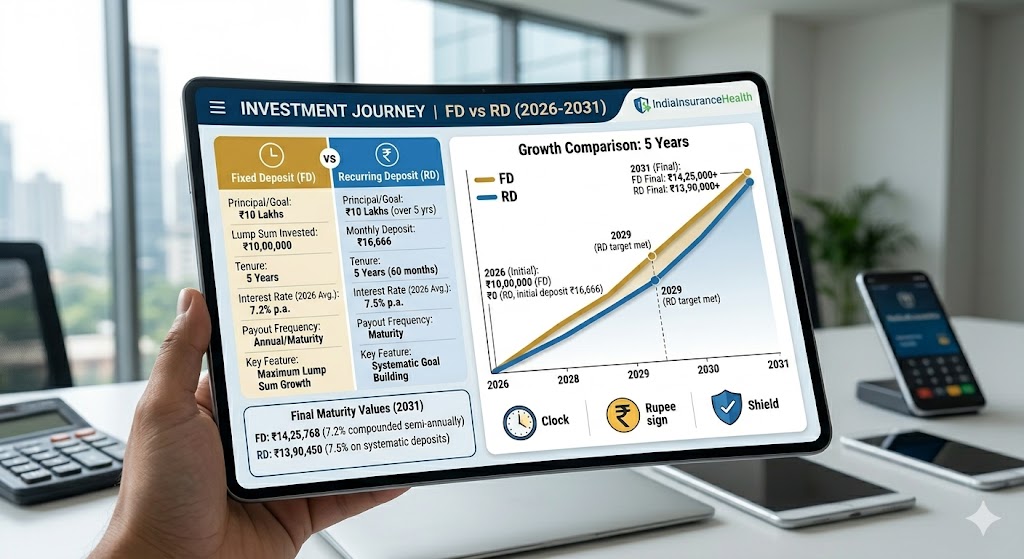

In the 2026 financial landscape, fixed-income instruments remain the cornerstone of low-risk investing for millions of Indians. Choosing between FD vs RD India 2026 depends entirely on your current cash flow. While both offer guaranteed returns and the security of DICGC insurance (up to ₹5 Lakh per bank), they serve different purposes. A Fixed Deposit (FD) is ideal for those with a “lump sum” sitting idle, whereas a Recurring Deposit (RD) is designed for salaried individuals looking to build a corpus through “monthly savings.”

Quick Comparison: FD vs RD India 2026

| Feature | Fixed Deposit (FD) | Recurring Deposit (RD) |

| Investment Mode | Lump Sum (One-time) | Monthly Installments |

| Interest Rate | Higher (Compounded on full amount) | Slightly Lower (Effective yield) |

| Ideal For | Windfalls, Bonuses, Idle Savings | Monthly Budgeting, Goal Building |

| Taxation | TDS on interest >₹40k/₹50k | TDS on interest >₹40k/₹50k |

| Liquidity | Premature withdrawal with penalty | Premature withdrawal with penalty |

1. The Interest Rate Gap in 2026

When looking at FD vs RD India 2026, the interest rates offered by major banks (SBI, HDFC, ICICI) are usually identical for the same tenure. However, the Total Interest Earned is always higher in an FD.

- Why? In an FD, the entire principal earns interest from Day 1. In an RD, only the first installment earns interest for the full tenure; the second installment earns for one month less, and so on.

- May 2026 Rates: Leading banks are offering 6.50% – 7.10% on 1-year tenures, while Small Finance Banks are touching 8.25% for senior citizens.

2. Flexibility and Discipline

- FD: Best if you have just received a bonus or a maturity payout from another scheme. It locks your money away so you aren’t tempted to spend it.

- RD: This is the “SIP of the banking world.” If you can save ₹5,000 every month after your salary is credited, the FD vs RD India 2026 choice clearly favors the RD to build discipline without needing a large upfront capital.

3. Taxation and TDS Rules

The tax treatment for FD vs RD India 2026 is now unified.

- TDS Threshold: Banks will deduct 10% TDS if your total interest across all deposits exceeds ₹40,000 (₹50,000 for senior citizens) in a financial year.

- Income Tax: The interest is added to your total income and taxed as per your slab (Old or New Regime).

Internal Resources

- To ensure you qualify for the best rates, check out our guide on how to improve CIBIL score in India 2026.

- If you need cash for an emergency after closing a card, see our loan without bank statement India 2026 guide.

External Resources

FAQ Section

1. Which gives more profit, FD or RD?

Mathematically, an FD gives more absolute profit because the entire amount is invested for the entire duration.

2. Can I change the RD installment amount mid-tenure?

Generally, no. In most 2026 banking products, the RD installment is fixed at the start. However, some banks offer “Flexi-RDs” where you can deposit surplus amounts.

3. Is interest from FD and RD tax-free in 2026?

No. Only the interest on a “Tax-Saving FD” (5-year lock-in) provides a deduction under Section 80C. Regular FD and RD interest is fully taxable.

Final Verdict

In the FD vs RD India 2026 debate, the “winner” is your habit. If you have the money now, go for an FD to maximize interest. If you want to save part of your monthly salary to reach a goal (like a vacation or a gadget), the RD is your best friend.