When it comes to securing your family’s financial future in India, one of the most critical decisions is understanding the difference between Term vs Life Insurance India. As the insurance landscape in India (2026) continues to evolve with more digitally accessible products, making an informed choice between pure protection and a combination of protection and savings is paramount.

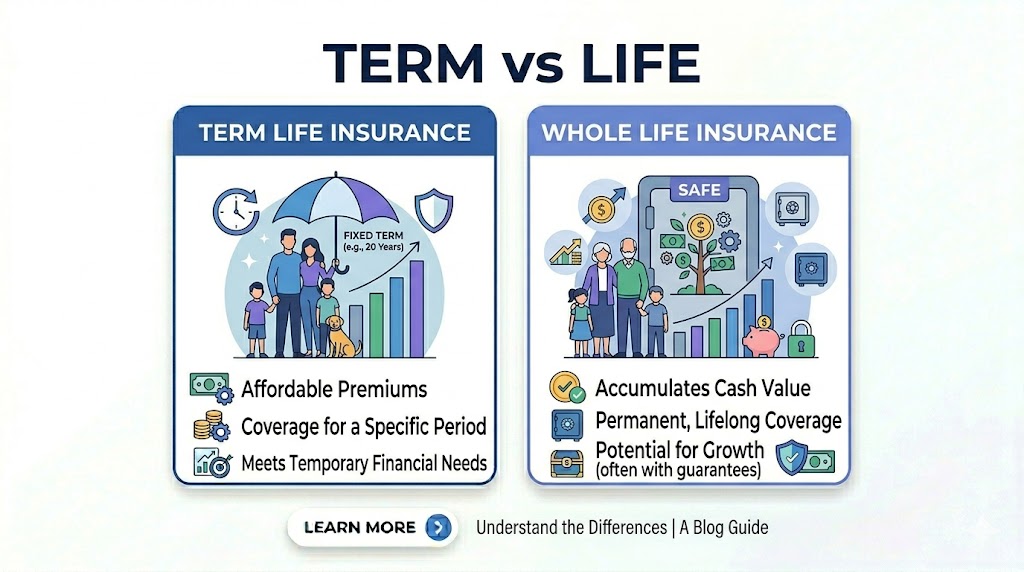

A term insurance policy is the simplest form of financial protection, designed to provide a high cover at an affordable cost for a specific duration. In contrast, “Life Insurance” in this context often refers to whole life or endowment policies that combine life cover with a savings component. Deciding between Term vs Life Insurance India hinges on your financial goals, budget, and the level of protection your dependents require.

Who is this for?

This comparison is vital for anyone in India looking to purchase a life insurance policy. It is particularly relevant for primary breadwinners, young professionals with dependents, and those looking to plan for long-term goals like a child’s education, retirement, or simply comprehensive financial security.

Best ways to Term vs Life Insurance India

The best approach to maximizing the benefits of Term vs Life Insurance India is to prioritize pure protection first. A standard Term Insurance plan should form the foundation of your financial plan to ensure maximum cover. If you have surplus funds and long-term savings goals, a dedicated investment instrument (like mutual funds) or a specialized Whole Life Insurance policy can supplement your pure cover.

Term vs Life Insurance India Comparison Table (2026)

| Feature | Term Insurance | Whole Life Insurance |

| Policy Nature | Pure Risk Cover | Risk Cover + Savings/Investment |

| Policy Term | Specific tenure (e.g., up to age 75 or 85) | Whole of Life (e.g., up to age 100) |

| Sum Assured | High (e.g., ₹1 Crore+) | Moderate (depends on premium) |

| Premium | Lowest among all life plans | Significantly higher (5x to 10x) |

| Maturity Benefit | None (unless return of premium plan) | Maturity Sum Assured + Bonuses |

| Surrender Value | Generally nil | Accrues over time (after 2-3 years) |

| Bonus | Not applicable | Reversionary or Terminal bonuses common |

Eligibility Criteria

To successfully complete the process for Term vs Life Insurance India, ensure you meet the following requirements:

- Age: Minimum entry age is generally 18 years; max varies (up to 65 for term, often lower for life).

- Resident: Must be an Indian resident or an NRI holding an Indian passport.

- Income: Regular source of income for term plans (proof required); life plans may allow single premiums.

- Health: Standard health required; pre-existing conditions may affect premiums or coverage.

Documents Required

- Identity & Address Proof: Aadhaar Card, PAN Card, or Passport.

- Income Proof (Term Insurance): Recent salary slips, 3 years’ ITR, or bank statements showing regular salary credits.

- Age Proof: Birth Certificate, 10th/12th Marksheet, or Passport.

- KYC Compliance: Recent color photograph and fully completed proposal form.

- Medical Reports: Mandatory medical check-ups may be required depending on age and sum assured.

Step by Step Process to Apply

- Assess Needs: Calculate the total sum assured your family requires based on liabilities, future needs, and income replacement.

- Compare Plans: Use the table above and online comparison tools to evaluate Term vs Life Insurance India across lenders.

- Fill Proposal Form: Provide accurate personal, professional, and medical details on the chosen insurer’s portal.

- Upload Documents: Submit digital copies of your KYC and income documents.

- Pay Premium: Choose your premium payment frequency (annual, monthly, single) and pay online.

- Medical Examination: Schedule the medical check-up (often home-based) if required by the insurer.

- Policy Issuance: Once the application passes underwriting, the policy document is issued via email/post.

Tips to Term vs Life Insurance India faster

To speed up the application process for Term vs Life Insurance India, always opt for an insurer offering an instant digital application path and disclose all medical conditions upfront to avoid underwriting delays.

Start Young to Get Lower Premiums

The most effective way to secure the best Term vs Life Insurance India rates is to purchase the policy as early as possible. Your health status is usually at its best when you are younger, which leads to lower risk for the insurer and significantly cheaper premiums for you. Buying a term plan in your 20s can lock in a low premium for the entire tenure.

Common Mistakes to Avoid

- Underinsurance: Opting for a low sum assured that does not cover actual needs.

- Hiding Medical Details: Concealing medical conditions can lead to claim rejection.

- Choosing ROP (Return of Premium): These often provide very low returns compared to pure term insurance.

- Treating Insurance as Investment: Focusing on returns rather than the primary goal of protection.

Safety Guidelines

Always choose insurers that are duly licensed and regulated by the Insurance Regulatory and Development Authority of India (IRDAI). When evaluating Term vs Life Insurance India, pay close attention to the Claim Settlement Ratio (CSR) of the insurer. Do not pay premiums through cash or unregulated third-party apps, and only share personal or financial information through the insurer’s official website or app.

Internal Resources to Improve Your Loan Approval

- Review Pre-approved Personal Loan in India: See how insurance history helps get loan offers.

- Learn how Loan for Low Income India is structured for diverse earners.

- Explore Loan Against Salary India: Another option for short-term needs.

Frequently Asked Questions

Is a Term vs Life Insurance India claim taxable?

Death benefits received from both types of policies are completely tax-free under Section 10(10D) of the Income Tax Act. Maturity benefits (for whole life) are also tax-free, subject to certain conditions regarding premium amounts.

Can I convert my term insurance to a life insurance plan later?

Some insurers offer convertible term plans that allow you to convert the policy into a whole life or endowment plan within a specific period without additional medical tests.

How is the premium for Term vs Life Insurance India determined?

Premiums are primarily based on your age, gender, sum assured, policy term, lifestyle habits (like smoking), and health status at the time of purchase.

What happens if I cannot pay the premiums for whole life insurance?

If you stop paying premiums for a whole life plan after it has acquired a surrender value (usually 2-3 years), it will not lapse but will continue as a ‘paid-up’ policy with a reduced sum assured.

Conclusion

Making the right choice between Term vs Life Insurance India is fundamental to your long-term financial security. A Term Insurance policy offers unparalleled pure protection with a high sum assured at a low cost, making it non-negotiable for breadwinners. However, if your protection needs are met and you seek a lifelong cover that also provides maturity benefits, a whole life plan may be suitable. Always base your decision on a comprehensive assessment of your family’s financial needs and future goals, and choose IRDAI-regulated insurers for maximum security.