In 2026, knowing How to Improve CIBIL Score in India 2026 is the absolute master key to your financial freedom. Your CIBIL score is a three-digit summary of your entire credit history, ranging from 300 to 900. For the 2026-27 period, banks have powerfully tightened their lending criteria, making a score of 750 or above a functional requirement for the best interest rates on home, car, and personal loans. A high score is a powerful signal to lenders that you are a reliable and trusted borrower.

The journey of How to Improve CIBIL Score in India 2026 is now seamless with the integration of real-time credit monitoring apps and instant dispute resolution portals. By applying effective credit habits, such as clearing outstanding dues and monitoring your credit utilization ratio, you can see absolute improvements in your score within a few months. Whether you are looking to recover from a past default or building credit from scratch, having a secure strategy is essential for a stable financial future.

Who is this for?

This guide is for anyone with a low credit score, those who have faced recent loan rejections, or young professionals looking to build a secure credit profile. If you want a functional and trusted way to boost your borrowing power in 2026, learning How to Improve CIBIL Score in India 2026 is for you.

CIBIL Score 2026: The “Gold Standard” Slabs

To How to Improve CIBIL Score in India 2026 effectively, you must understand where you stand in the absolute eyes of 2026 lenders:

| Score Range | Category | Impact on Loans (2026) |

| 750 – 900 | Excellent | Instant approval; Lowest interest rates. |

| 700 – 749 | Good | High approval chances; Standard rates. |

| 600 – 699 | Average | May require collateral; Higher rates. |

| 300 – 599 | Poor | High risk of rejection; Requires absolute repair. |

2026 Strategy: For the absolute fastest recovery, prioritize clearing any “Settled” or “Written-off” accounts in your report to turn them into “Closed” status.

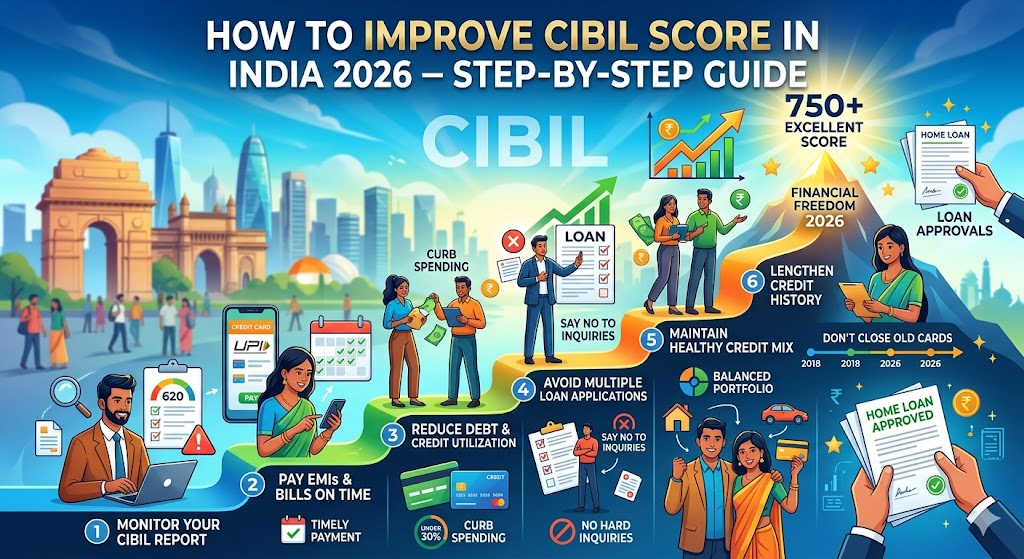

5 Powerful Steps: How to Improve CIBIL Score in India 2026

To get your score moving upward instantly, follow this effective digital journey:

- Audit Your Report: Download your trusted CIBIL report and check for absolutely any errors in your name, PAN, or account statuses.

- The “30% Rule”: Maintain your total credit card usage below 30% of your limit. This shows functional credit discipline to the bureaus.

- Automate Payments: Set up secure standing instructions for all EMIs and credit card bills. Even a one-day delay can cause an instant score drop.

- Avoid Multiple Inquiries: Don’t apply for multiple loans simultaneously. In 2026, “Hard Inquiries” stay on your record and signal a functional hunger for credit.

- Mix Your Credit: Maintain a healthy balance between secure loans (Home/Gold) and unsecured loans (Personal/Credit Card) for absolute profile strength.

Tips for a Successful Credit Recovery

To make your recovery truly valuable, keep your oldest credit card accounts active; the length of your credit history is a functional driver of a high score. Additionally, checking our guide on Best Credit Cards in India for Beginners 2026 can help you find “FD-backed” cards that are powerfully effective for rebuilding credit. For those who need to consolidate debt, reviewing Personal Loan Eligibility in India 2026 can provide a way to pay off high-interest cards. If you are starting fresh, opening a Best Savings Account in India 2026 with a bank you trust can lead to pre-approved credit offers. For long-term goals, starting a How to start SIP in India 2026 helps build the wealth needed to stay debt-free.

The “Credit Mix” Mastery

In 2026, bureaus powerfully reward those who manage different types of credit. Having a small gold loan or a consumer durable loan alongside a credit card proves you can handle diverse financial responsibilities absolutely.

Common Mistakes to Avoid

- Closing Old Cards: This reduces your “Age of Credit,” which is an absolutely vital factor for a high score.

- Ignoring Errors: A single wrong entry on your PAN can tank your score. Use the secure CIBIL dispute portal instantly to fix mistakes.

- Paying Only “Minimum Due”: While this avoids late fees, it keeps your utilization high and interest ballooning, which is not a functional long-term strategy.

Related Financial Resources

- Personal Loan Eligibility in India 2026: Consolidate debt to save your score.

- Best Credit Cards in India for Beginners 2026: Cards that help you build credit.

- How to open zero balance account in India 2026: Clean banking for a clean credit start.

Frequently Asked Questions

Can I improve my CIBIL score in 30 days?

You can’t get an absolute overhaul in 30 days, but paying off a large credit card balance can show a functional jump in your score in the next reporting cycle.

Does checking my own CIBIL score reduce it?

No. In 2026, self-checks are “Soft Inquiries” and have absolutely zero impact on your score.

How much does one late payment affect CIBIL?

A single late payment can cause an instant drop of 50-100 points, making consistency a functional priority.

How to improve CIBIL score if I have no credit history?

The fastest way is to get an FD-backed credit card or a small consumer durable loan to start your trusted record.

Conclusion

Mastering How to Improve CIBIL Score in India 2026 is a crucial step for anyone looking to access better financial opportunities and credit products. Understanding How to Improve CIBIL Score in India 2026 helps you build a strong credit profile that lenders trust.

By following disciplined repayment habits, maintaining low credit utilization, and keeping your credit report accurate, you can effectively implement How to Improve CIBIL Score in India 2026 strategies. A clean and well-managed credit history is key to improving your score and unlocking premium loans and credit cards.

To succeed with How to Improve CIBIL Score in India 2026, regularly monitor your credit report, correct errors promptly, and ensure timely payments on all credit accounts. A proactive approach to How to Improve CIBIL Score in India 2026 ensures steady improvement and long-term financial credibility.

By mastering How to Improve CIBIL Score in India 2026, you can confidently navigate the credit ecosystem, access better interest rates, and build a strong financial future while staying aligned with RBI guidelines.